EdTech hits $2.6B in investment as the market stabilizes. Bigger bets in AI and workforce training.

$2.6B in EdTech investment in 2025 underscored a market settling into steadier ground, backing solutions that demonstrate traction while advancing employability and AI-enabled learning.

2025 saw $2.6B of EdTech investment underscoring a market settling into steadier ground, backing solutions that demonstrate traction while advancing employability and AI-enabled learning.

Funding did not return to the highs of 2020–2021, nor did it repeat the sharp contraction of 2023. Capital concentrated around companies demonstrating two things simultaneously: credible market traction and innovation, especially in AI-enabled platforms and solutions tied directly to employability. Investment rose roughly 11% over 2024, but the tone of the market was far from exuberant. Pricing stayed disciplined, investors pushed for profitability, and companies demonstrating real demand signals captured the bulk of attention. The market story of 2025 is one of pragmatism as investors and acquirers look for products that solve discrete problems and have sustainable paths to revenue.

Figure 1. Global EdTech VC Funding. 2010 - 2025

No items found.

Venture capital: less about volume, more about intention

Venture capital flows reflected a shift from volume to intention. Deal counts held relatively steady, yet nearly 40% of all transactions sit above the $5M mark. Early-stage activity eased slightly but still represented about 87% of total deal volume, consistent with 2024. Investors concentrated capital in AI-enabled products, workforce-aligned platforms, and K–12 operations solutions that address cost or operational pressures, staffing challenges, and learning support at scale.

Capital followed clear demand signals rather than predominately experimental hype. In upskilling and health training, shortages and credentialing needs created immediate market opportunity. In K–12, solutions that reduced administrative burden and improved operational efficiency drew investor interest, reflecting district pressure to do more with constrained resources.

Examples that stood out included Synthesia, continuing to draw attention as AI video creation moved further into enterprise learning and training workflows, and Sana, which was acquired for $1.1B by Workday, is gaining traction as an AI-powered knowledge and learning platform inside companies. These raises were anchored in use cases already in motion, not hypothetical future growth.

Examples that stood out included Synthesia, which continues to attract attention as AI video creation expands into enterprise learning and training workflows, and Sana, acquired by Workday for $1.1B. These deals were driven by active use cases and desired capability building rather than speculative future growth.

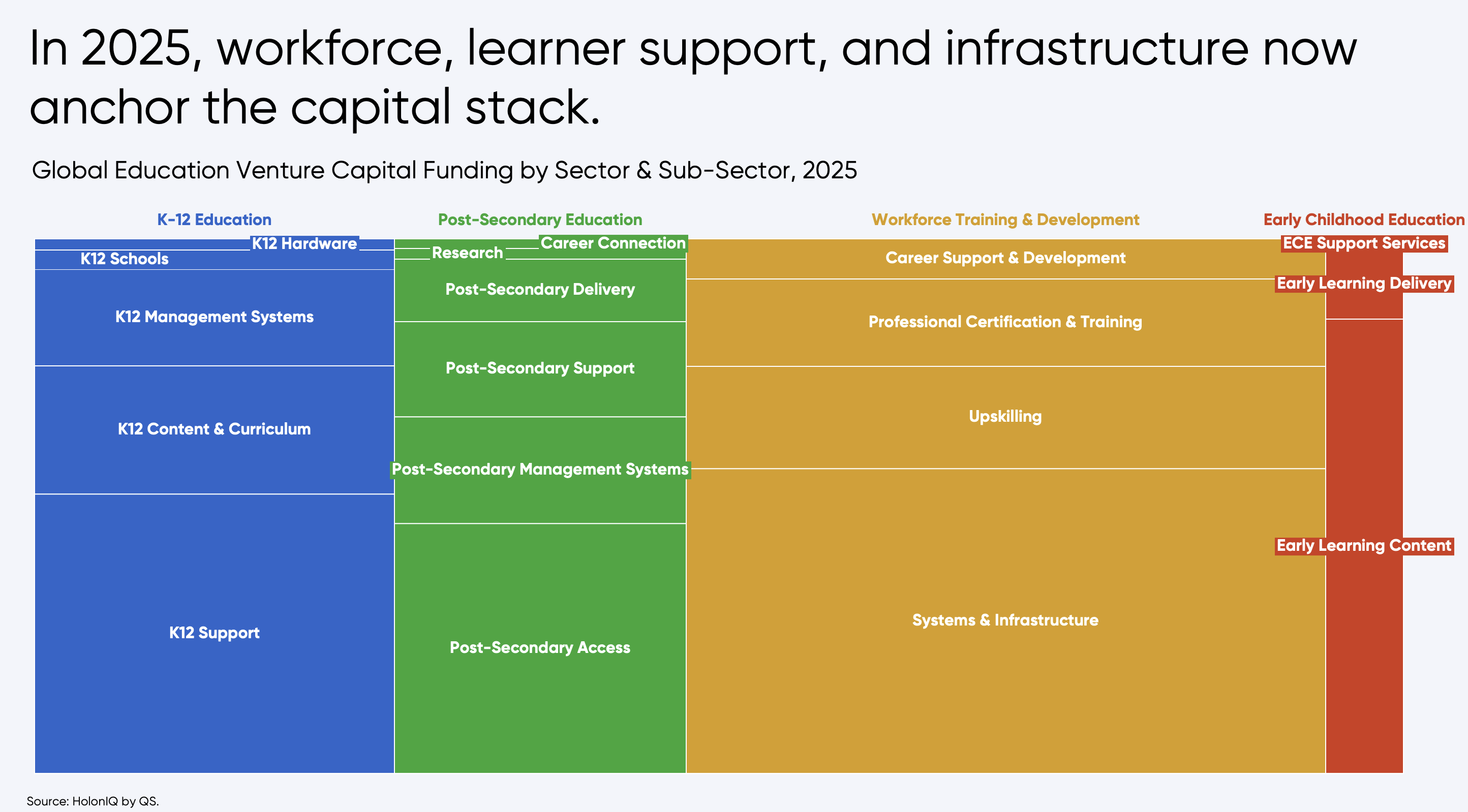

Sector patterns in 2025 largely mirrored last year, with workforce training and development again the largest category at 38% of deal volume, followed by K–12 at 36%, post-secondary at 22%, and early childhood at 4%. Capital concentrated around enterprise tools such as cybersecurity and upskilling platforms, including platforms such as Simspace’s $39M, reflecting continued demand for job-aligned learning infrastructure. K–12 activity remained strong in tutoring, curriculum, and school operations, with notable rounds such as Starbridge’s $42M and MagicSchool AI’s $45M. Post-secondary investment held steady across access, navigation, and engagement tools, with investments such as Leap Scholar’s $65M. Across sectors, investors favored digitally integrated systems that sit inside institutional and employer workflows: LMS, assessment, finance, and data platforms, a trend underscored by Instrumentl’s $55M raise. Expect capital in 2026 to remain disciplined, with preference for workflow-embedded, agentic AI integrated platforms, and solutions that deliver measurable and well-defined outcomes.

Figure 2. Global Education Venture Capital Funding by Sector & Sub-Sector, 2025

Ready to get started?

Get a personalized walkthrough of HolonIQ's Global Intelligence Platform.

M&A: Education is hybrid. Digital upskilling & school delivery in focus.

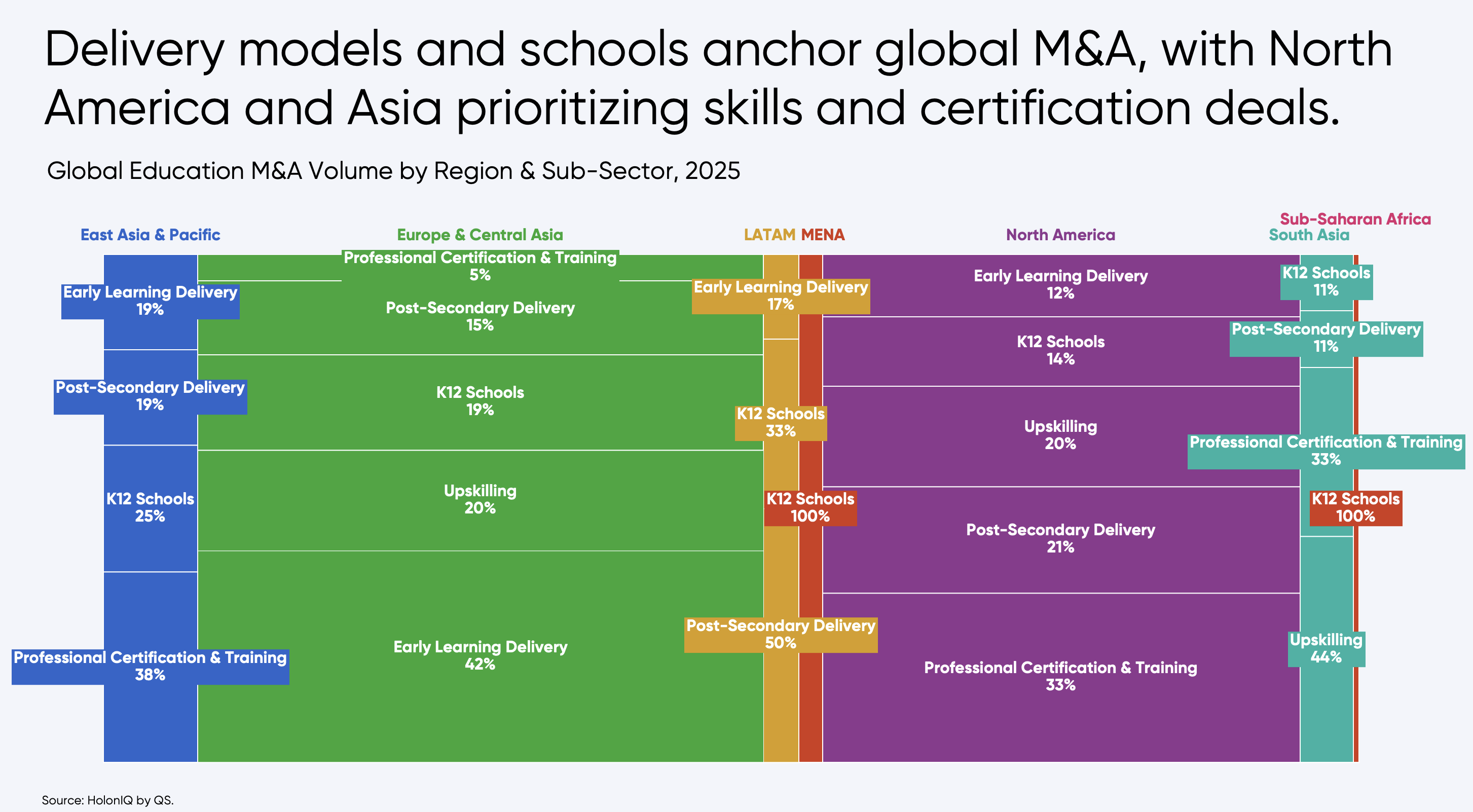

Transaction volume increased in 2025, with acquirers focused on physical delivery assets across regions, including schools, childcare facilities, and universities. Examples included Brightstar Capital Partners’ purchase of Arden University and continued consolidation across early learning providers, where deal activity rose more than 30%. These transactions reflected continued demand for school- and delivery-focused assets, particularly where operating footprints and enrollment pipelines could be scaled.

At the same time, digital workforce solutions were a primary global target. Around one-third of all transactions were in workforce training, centered on systems and infrastructure providers and upskilling platforms. Notable examples included Workday’s acquisition of Sana and Coursera’s acquisition of Udemy, both reinforcing the emphasis on employability, enterprise learning, and AI-enabled capability building. Acquisitions also extended into AR/VR tools, work-integrated learning models, and lifelong learning platforms. Overall M&A activity reached about 410 transactions in 2025, including 22 private equity acquisitions, up about 20% from 2024.

Figure 3. Global Education M&A Volume by Region & Sub-Sector, 2025

No items found.

Latest Insights

Global Insights from HolonIQ’s Intelligence Unit. Powered by our Global Impact Intelligence Platform.

We provide you with relevant and up-to-date insights on the global impact economy. Choose out of our newsletters and you will find trending topics in your inbox.