Against a backdrop of geopolitical tension, uneven economic signals, and fluctuating global markets, EdTech investment continued, but with noticeably tighter discipline around where capital flowed and how much risk investors were willing to carry.

Venture funding in Q1 reached $512M across 63 deals, reflecting a 24% decline in value and a 10% decline in volume compared with Q1 2025. The decline wasn’t driven by waning interest so much as by fewer large rounds clearing the market, as investors remained selective in a year where uncertainty continues to shape decision‑making well beyond the education industry.

For education stakeholders, this matters less as a headline and more for what it implies operationally: a more uneven vendor landscape, with some platforms well-capitalised and others likely operating with tighter margins and shorter runways.

Figure 1. Global Education Venture Capital Funding, 2010-Q1 2026

Workforce solutions draw continued attention, powered by AI.

The clearest signal in venture capital came from workforce language learning solution Preply’s $150M raise, the largest round of the quarter, suggesting investors were willing to write checks where demand is global, outcomes are job‑aligned, and usage is repeatable. By contrast, other activities skewed earlier stage. Guidde’s $50M stood out as another meaningful exception, reflecting continued appetite for AI‑enabled tools that support 360 talent solutions that serve multi-purposes such as onboarding, enablement, upskilling and productivity inside organizations rather than introducing new learning models that require buyers to change behaviour. Capital seems to be gravitating toward platforms already embedded in day‑to‑day work and training environment, particularly those that are getting enhanced and upgraded with AI. Expect sharper differentiation between vendors with scale and those still proving durability.

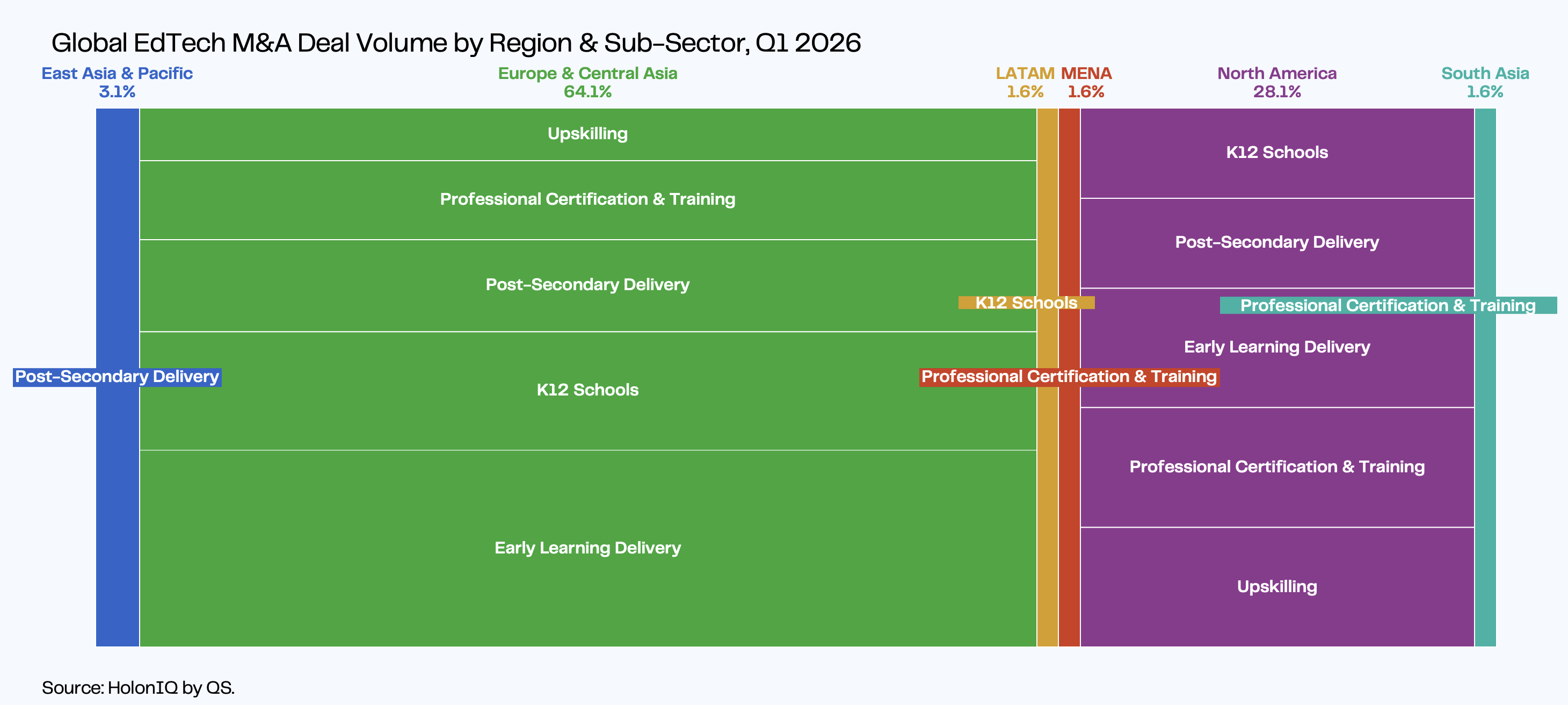

Across sectors, investment concentrates in learner support, upskilling, system-wide solutions, with content increasingly in focus in K-12 and Early Learning.

Figure 2. Global Education Venture Capital Funding by Sector & Sub-Sector, Q1 2026