The Latin American EdTech 100 is HolonIQ's annual list of the most promising EdTech startups from the region.

The Latin America EdTech 100 is focused on identifying young, fast growing and innovative learning, teaching and up-skilling startups from the region. Powered by data and insights from our Impact Intelligence Platform together with qualitative assessments by HolonIQ’s Intelligence Unit, and local market experts, organizations are evaluated and scored based on our eligibility and assessment criteria, which excludes EdTech's founded over 10 years ago, or those which have exited (listed, acquired or controlled by another organisation).

The LATAM EdTech 100 is aligned to the Global Learning Landscape, an Open-Source Taxonomy that maps the education and talent market

Latin America’s EdTech Market is Evolving.

The 2025 Latin America EdTech 100 highlights the region’s most promising startups in education technology, and this year’s cohort reflects a dynamic but maturing ecosystem strong in Workforce and K-12, where systems, support, and skills remain central. While the market continues to prioritize scalable solutions, a younger generation of startups is beginning to emerge—signaling the early stages of a new innovation cycle.

Exhibit 2. Alignment with the Global Learning Landscape Taxonomy

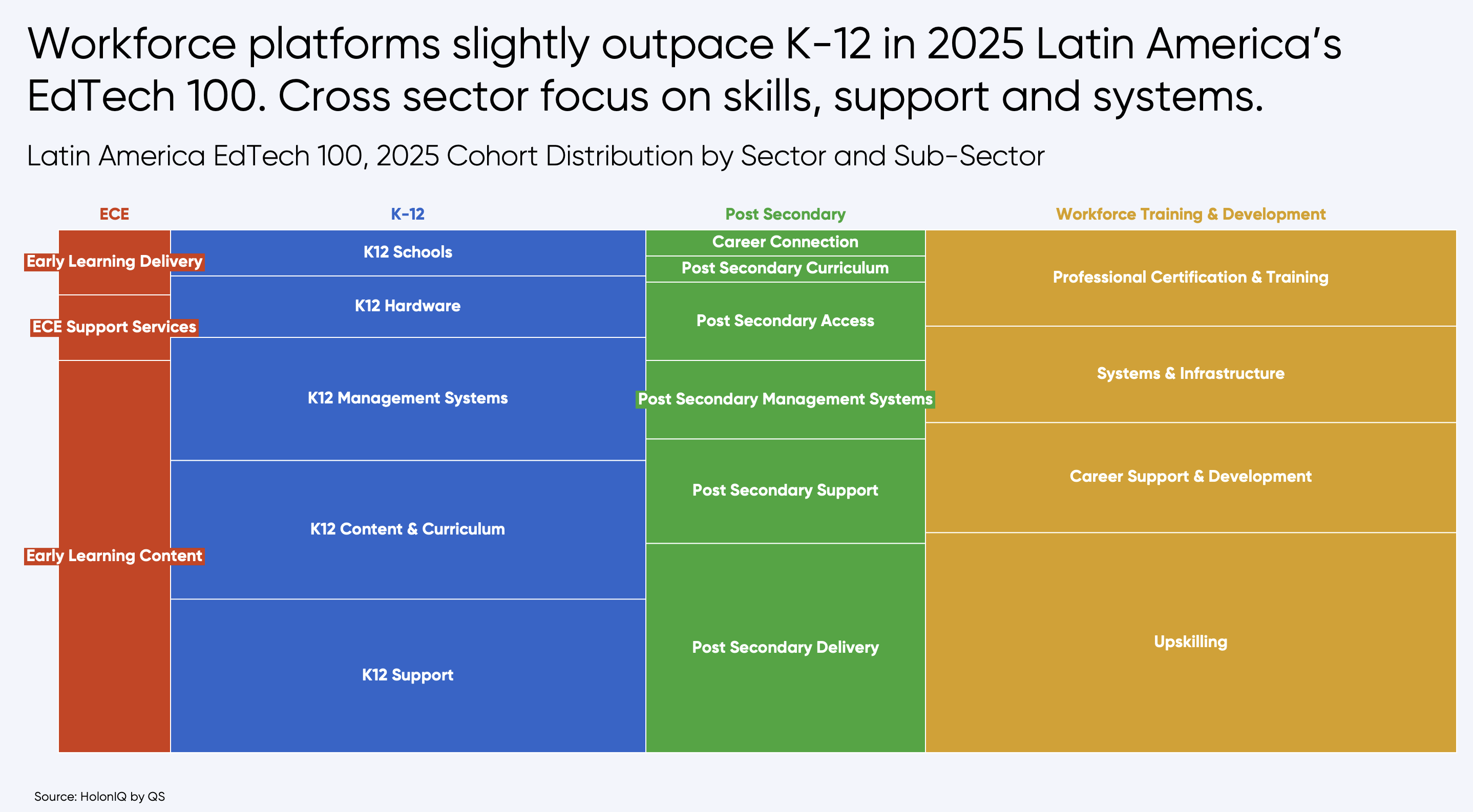

Workforce and K–12 remain central to the region.

Workforce platforms slightly outpace K–12 in this year’s cohort, but both remain central to the region’s EdTech landscape. Argentina’s Edison and Brazil’s Ada Tech stand out in the workforce space, part of a growing group of platforms focused on career-aligned learning. The data shows a continued emphasis on skills, support, and systems across sectors, reflecting a pragmatic approach to innovation that serves both institutions and individual learners.

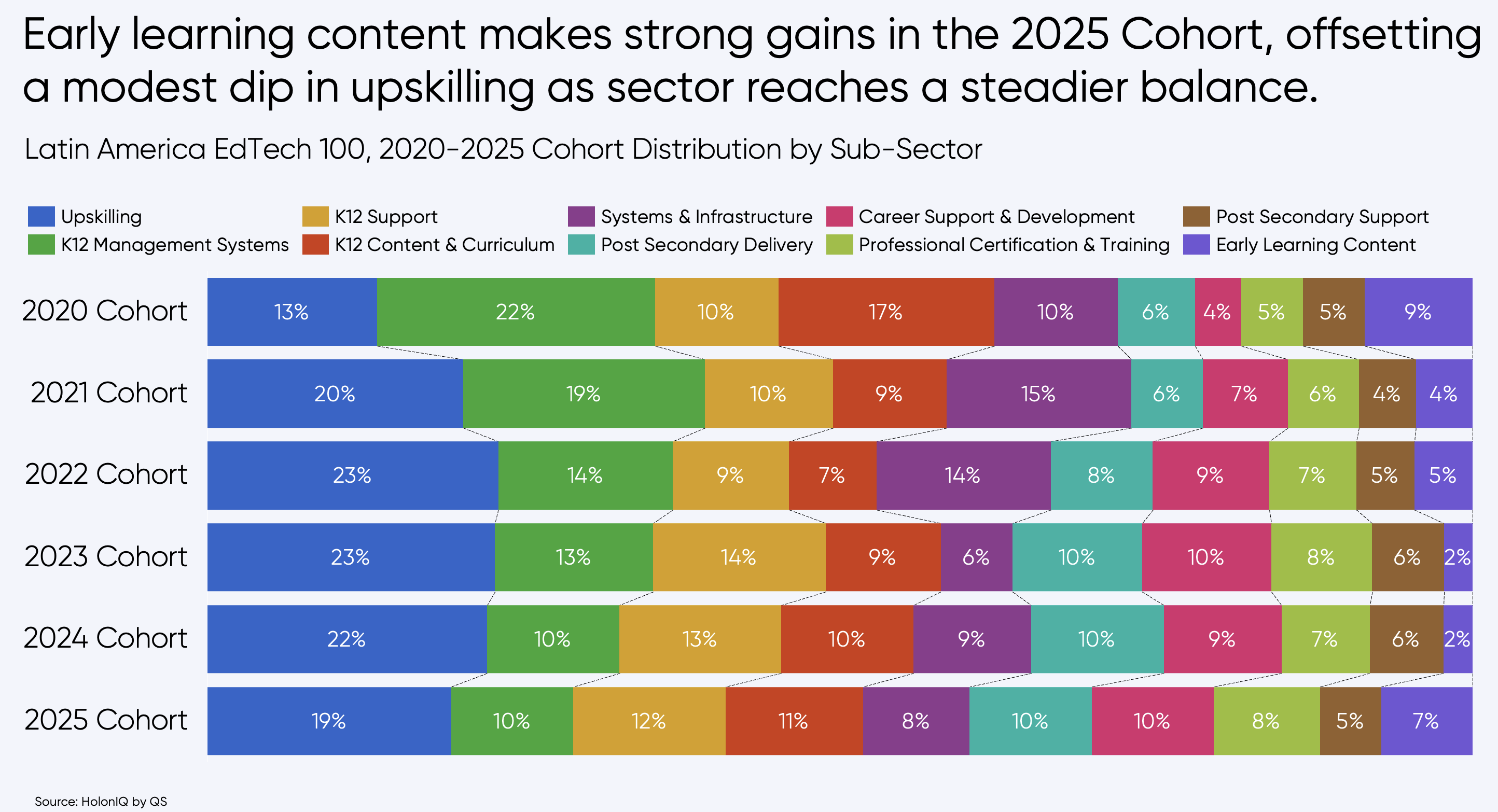

Early Learning content gains ground.

Subsector distribution shows a notable rise in Early Learning Content, offsetting a modest dip in upskilling (from nearly taking a quarter of the cohort in 2023). Brazil’s Yuna raised $1.6M as part of this momentum, contributing to the growing attention on foundational education. Alongside other early childhood innovators, Yuna, as well as other ECE content providers in the list (Escribo), reflects a broader shift toward engaging, accessible tools that support early literacy and learning—an area gaining traction globally.

Exhibit 3. Cohort Distribution by Sub-Sector 2020-2025

Ready to get started?

Get a personalized walkthrough of HolonIQ's Global Intelligence Platform.

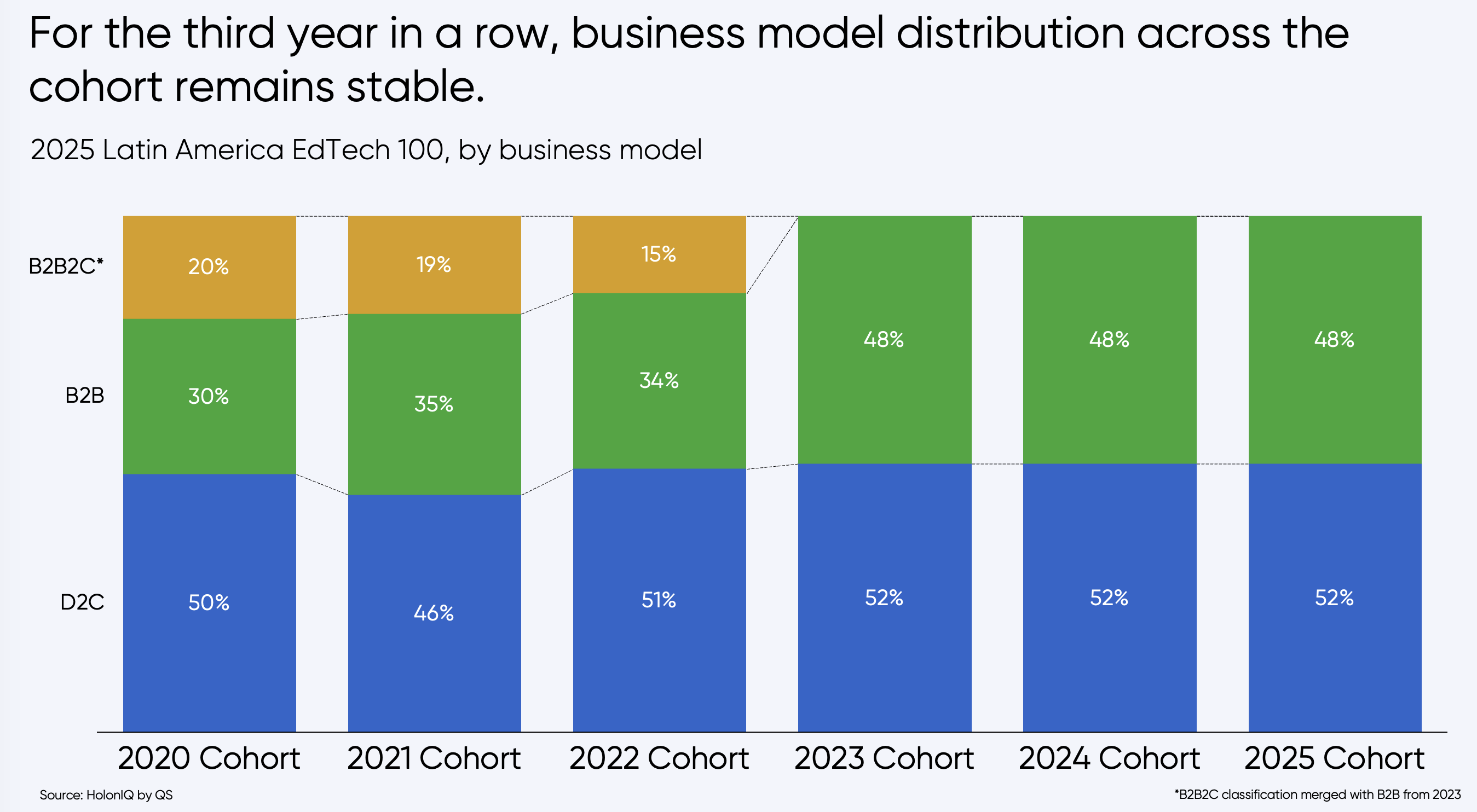

Business models remain balanced as the EdTech market matures.

For the third year running, business model distribution remains stable, with Direct-to-Consumer (D2C) continuing to dominate. B2B models also maintain a strong presence, particularly in infrastructure and financing education EdTechs; for example, Mexico’s Cometa, operating in the B2B space, raised $12M this year. At the same time, the age profile of the cohort is shifting. Startups such as Brazil’s Principia Educação, which also had a significant cash injection, is a part of a more seasoned middle tier that’s setting the pace for growth and execution. The market is rewarding clarity, traction, and staying power, especially as younger players navigate a competitive but capital-conscious environment.

Exhibit 4. Cohort Distribution by Business Model, 2020-2025

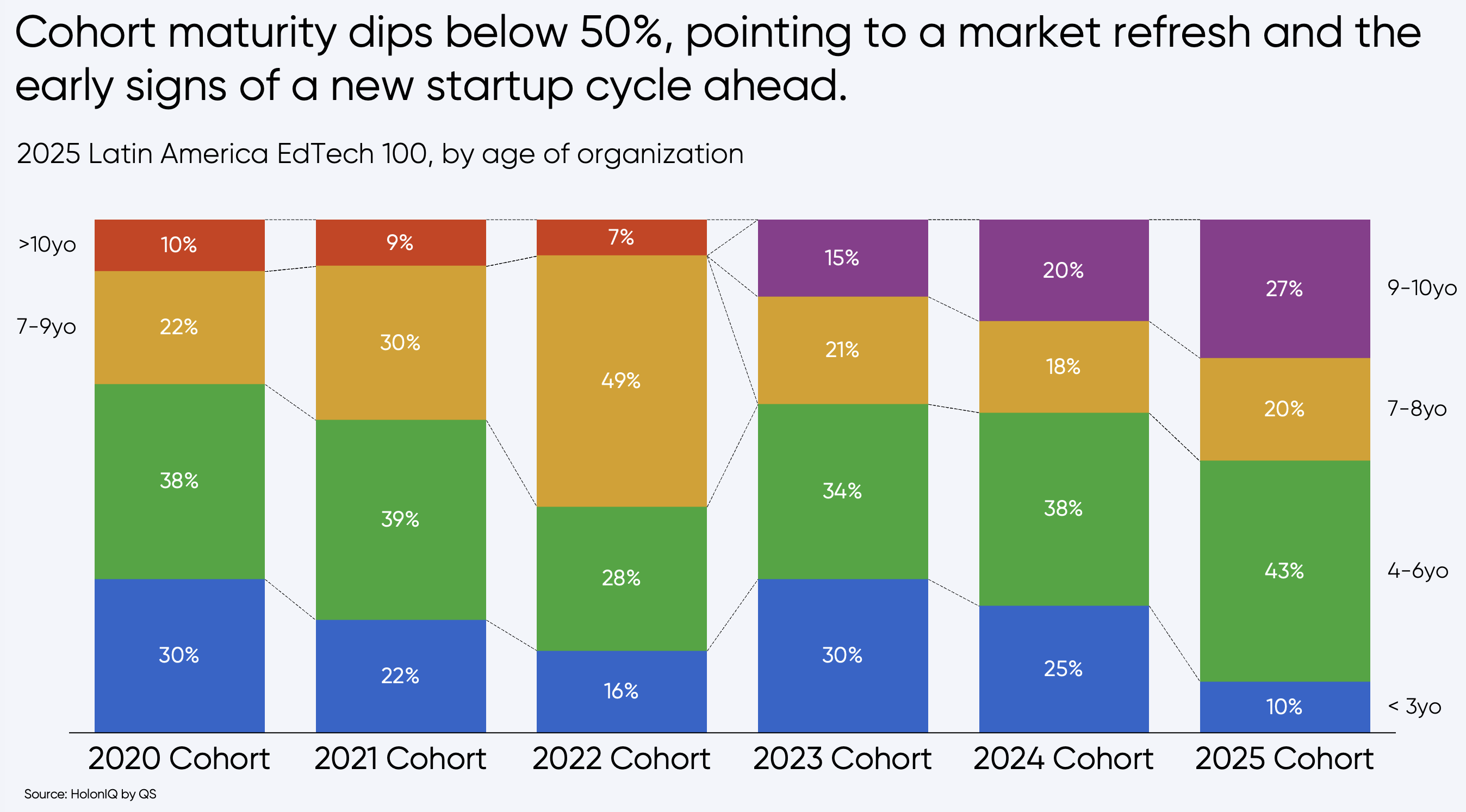

A younger cohort signals market refresh.

Cohort maturity has dipped below 50%, with a growing share of startups under three years old. This shift could point to a broader refresh in the market. New entrants like Peru’s Incluedu, AI-Powered platform making sign language learning interactive, accessible, and inclusive, are emblematic of this early-stage energy, bringing fresh thinking to long-standing challenges. The balance of early- and mid-stage companies suggests a healthy pipeline of innovation, even as funding conditions remain tight.

Exhibit 5. Cohort by Age Distribution, 2020-2025

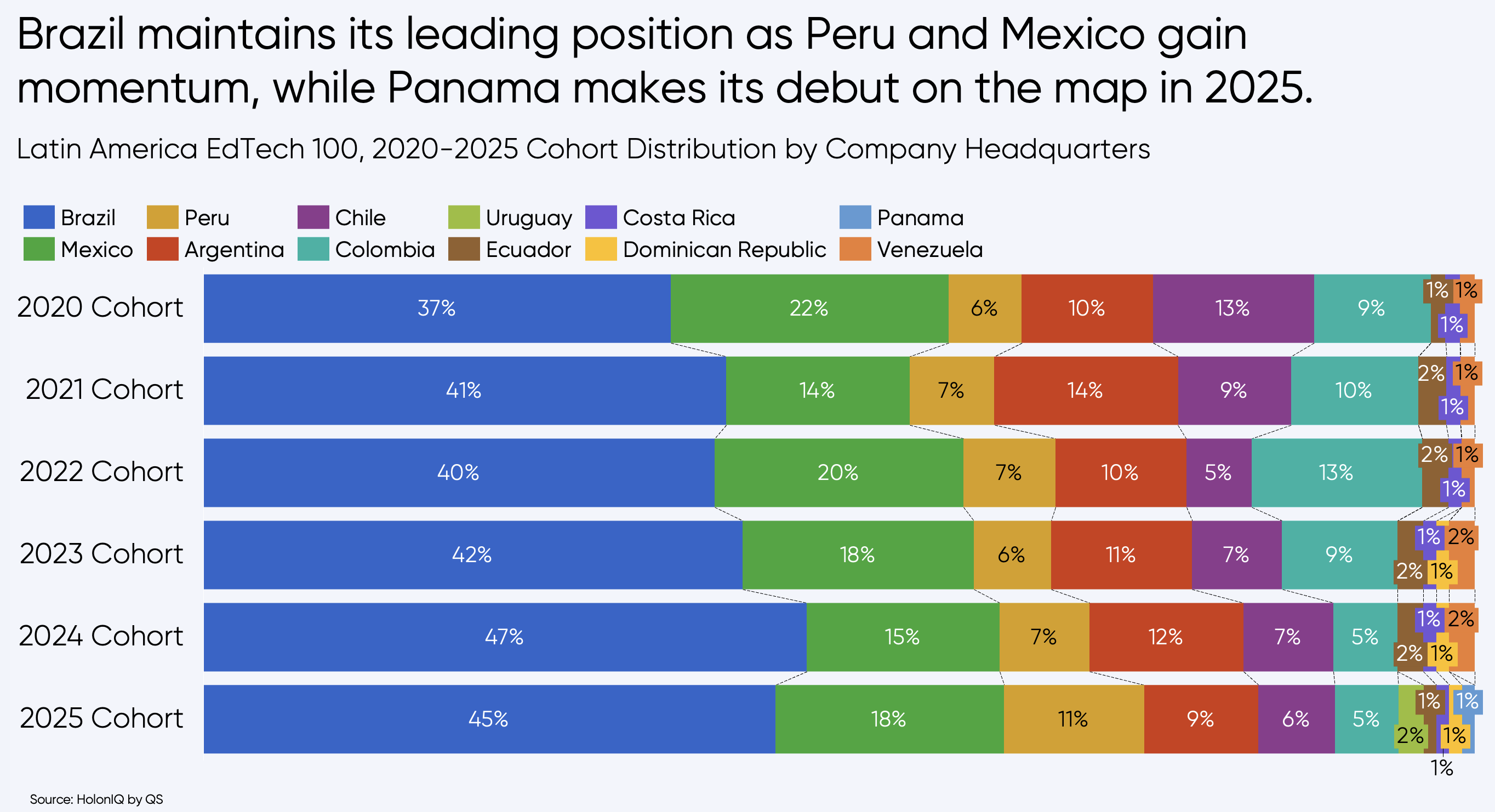

Brazil holds almost half of the 2025 Cohort, but the map is shifting.

Brazil continues to anchor the region’s EdTech landscape, accounting for 45% of this year’s cohort. But the map is slowly diversifying. Mexico has gained ground, now representing 18% of the list, while Peru shows growing momentum with a new wave of startups entering the scene. Panama makes its first appearance in the cohort, signaling the emergence of new innovation hubs across the region. This evolving distribution reflects a broader decentralization of EdTech activity, as more countries build out their ecosystems and attract early-stage talent and capital.

Exhibit 6. Cohort Distribution Geography, 2020-2025

Track the 2025 Cohort

HolonIQ customers can track the data for the most promising EdTech startups in the region on the HolonIQ Intelligence Platform. Look for the 2025 LATAM EdTech 100 list and double click into the data behind the charts. Request a Demo if you are not a customer and would like to learn more.

No items found.

Latest Insights

Global Insights from HolonIQ’s Intelligence Unit. Powered by our Global Impact Intelligence Platform.

We provide you with relevant and up-to-date insights on the global impact economy. Choose out of our newsletters and you will find trending topics in your inbox.

.png)