$1B in EdTech Venture Capital for 1H. Funding falls short of last year’s midpoint. Asia & MENA buck the trend.

Overall EdTech VC funding fell 26% year-over-year, yet certain sectors and geographies made gains. East Asia deal volume climbed 37% and Early Childhood Education more than tripled its 2025 deal count, signaling investor appetite in specific corners of the market.

For 1H, overall EdTech venture funding fell 26% year-over-year, yet certain sectors and geographies made gains. East Asia deal volume climbed 37% and Early Childhood Education more than tripled its 2025 deal count, signaling investor appetite in specific corners of the market.

Venture funding totalled $1B in H1 2026, a 26% decrease from the $1.35B recorded in H1 2025. Deal volume remained stable suggesting investor activity and appetite for EdTech persists even as average deal sizes contract.

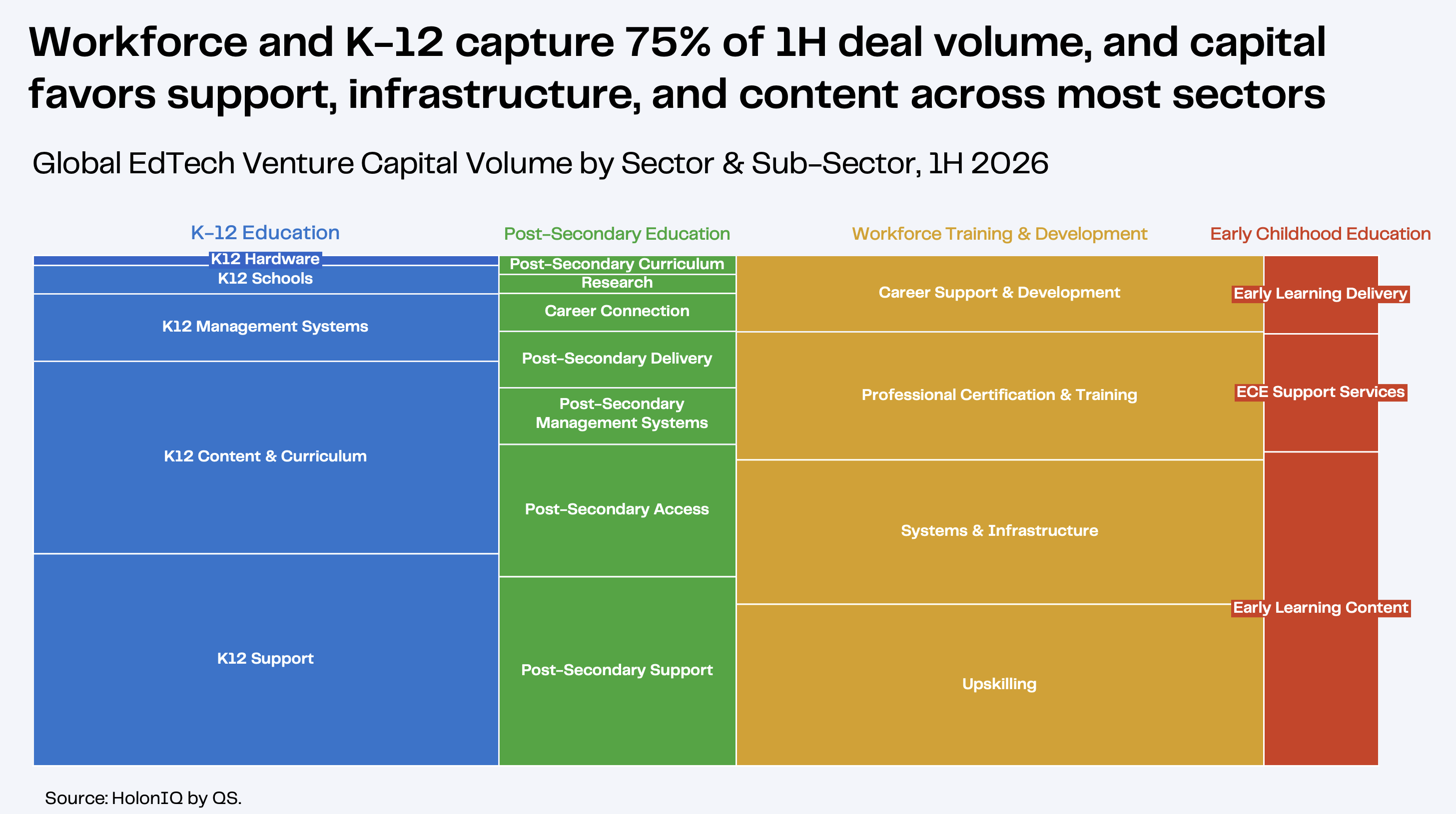

A closer look at the data reveals several bright spots. Workforce Training and Development continued to attract the majority of funding, with notable raises including Preply's $150M round and Multiverse's at $70M. These companies exemplify the growing demand for tech-enabled upskilling and reskilling solutions as employers grapple with talent skill shortages.

Figure 1. Global EdTech VC Funding. 2010 - 1H 2026

No items found.

Venture capital: pockets of strength amid broader cooling

In K-12, AI-enabled personalization solutions gained traction, with companies such as Subject and Gizmo securing significant funding to bring direct learning capabilities to more learners and classrooms. Post-secondary saw sustained interest in alternative credential providers and work-integrated learning models, even as overall funding dipped.

Figure 2. Global EdTech Venture Capital Volume by Sector & Sub-Sector, 1H 2026

Ready to get started?

Get a personalized walkthrough of HolonIQ's Global Intelligence Platform.

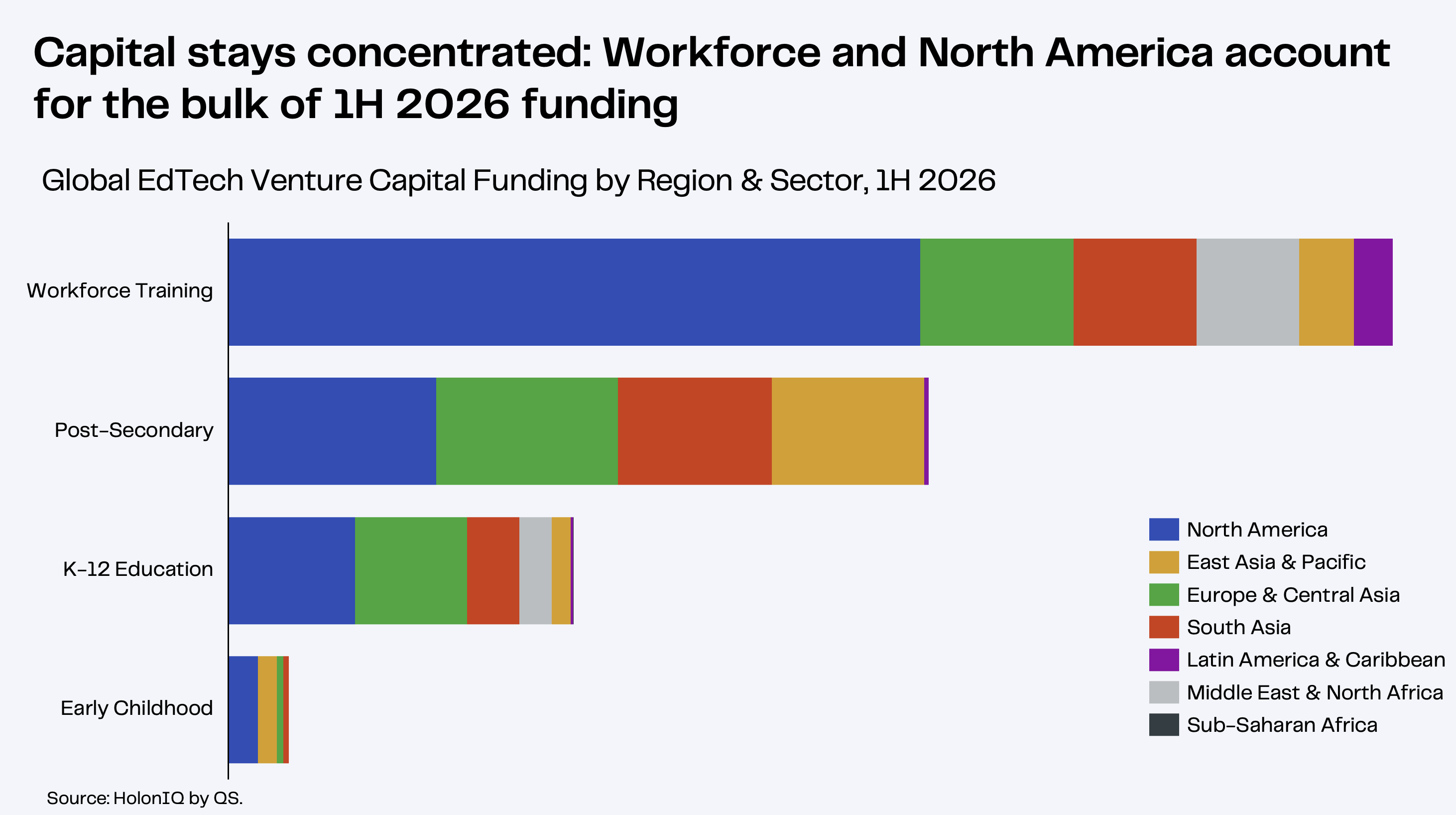

The U.S. and Europe remained the top regions for EdTech investment, with the former attracting large workforce deals and the latter seeing activity in learning delivery and corporate training. China showed early signs of a rebound following a period of regulatory turbulence.

M&A momentum

Workforce Training & Development held flat in deal count but shrank as a share of the M&A mix, from 37% to 25%, while K-12, post-secondary, and early childhood all grew. It looks like a rotation toward institution- and learner-facing assets, but it’s still too early to call it a trend.

Private equity growth capital investment climbed in volume even as value dipped: 17 deals in H1 2026 versus 10 in H1 2025. Total capital fell from $445M to $290M, a reflection of last year's outlier, XCL Education's $400M raise, rather than any retreat in investor interest..

K-12 Education still drew the largest share of PE growth capital, with Zum's $100M raise and Minga's $65M round, though its share of deal volume eased from 80% to 53% as capital diversified into Post-Secondary Education, including BibliU's $55M, and Workforce Training & Development. North America led the activity, with deal count volume rising from 30% to 65% from 2025 to 2026.

The road ahead

As we head into the second half of 2026, investors will still be waiting on the returns from pandemic-era bets, even as the fundamental drivers of technology adoption in education remain strong.

Until those returns materialize, expect investors to stay focused on companies that can deliver measurable outcomes and ROI for learners and institutions. From AI-powered personalization to immersive learning experiences, the technologies poised to reshape education are those that can tangibly improve access, engagement, and outcomes.

At the same time, the skills gap continues to loom large over the labor market, fueling demand for innovative upskilling and reskilling solutions. Edtech companies that can bridge the divide between education and employment will be well-positioned to capture market share and investment.

As the sector evolves, one thing is clear: the future of learning will be data-driven, and focused on real-world outcomes, and will include digital—despite growing concerns over screentime use and social media with young learners. The investors and entrepreneurs shaping that future will likely be those who can navigate the complexities of an ever-changing market while staying true to the mission of empowering learners and educators worldwide.

We provide you with relevant and up-to-date insights on the global impact economy. Choose out of our newsletters and you will find trending topics in your inbox.