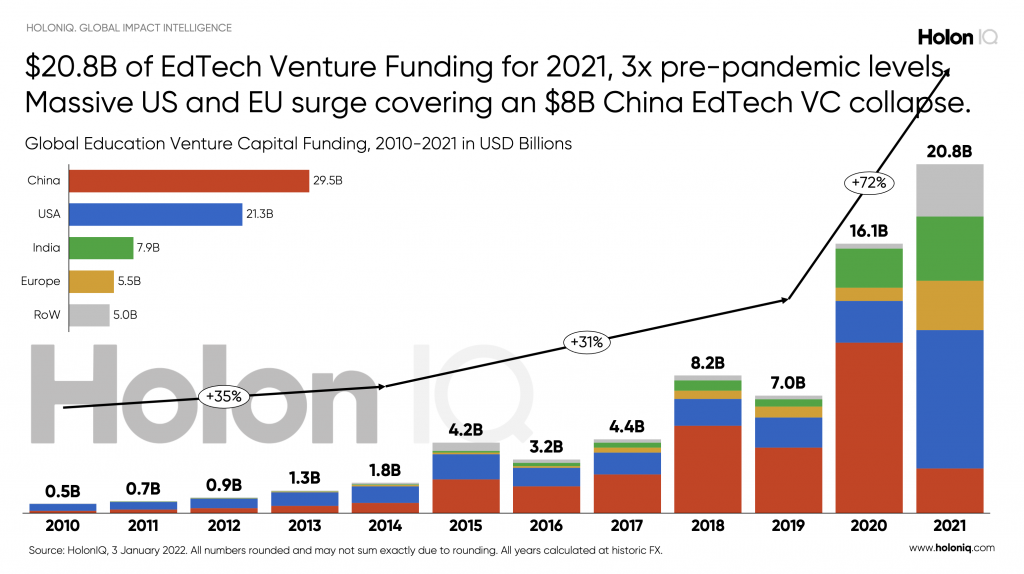

EdTech Venture Capital reached 3x pre-pandemic investment levels in 2021, accelerating startups around the world with over $20B of funding. Fueled by a massive US and EU investment surge and India's growth charging onwards, collectively global growth covered an $8B investment collapse from China and managed to set record growth for the sector.

As we reluctantly enter the third year of the pandemic, EdTech is powering students and parents, schools and teachers, professors and institutions, governments and employers around the world with critical tools, content, processes and learning outcomes to mitigate learning loss through the pandemic and accelerating up-skilling into a new labor economy.

Once a niche sector with an ambitious vision to transform the way the world learns, EdTech Venture investment is now 40x larger than it was a little over a decade ago in 2010, nearly 5x the previous investment peak in 2015 and 3x pre-pandemic investment levels in 2019. With innovation surging across the entire EdTech Landscape notable mega rounds included 🇺🇸 Articulate‘s $1.5B Series A, 🇮🇳 Eruditus‘ $650M Series D, 🇮🇳 Unacademy‘s $440M Series H, 🇨🇳 Fenbi‘s $390M Series A, 🇺🇸 Course Hero‘s $380M Series C, several $300M rounds in 🇺🇸 Better Up‘s Series C, 🇺🇸 Age of Learning‘s Series C and 🇨🇦 ApplyBoard’s Series D, 🇦🇹 GoStudent‘s $244M Series C and 🇺🇸 Masterclass‘ $225M Series F.

With 32 EdTech Unicorns at the end of 2021, 61 Mega Rounds ($100M+) over the last 12 months and now more than 3,000 funding rounds over $5M in EdTech’s history, this cumulative wave of investment in innovation and technology marks a meaningful milestone in the digital transformation of learning from early childhood though school, college and university to a new approach from industry for up-skilling and lifelong learning.

No items found.

China's EdTech investment collapse was offset with an incredible surge in investment in the US and across Europe. India is now Asia's investment leader in education, surpassing Europe as a whole, yet less diversified.

2020 set a new EdTech record by China, investing over $10B of venture capital into the sector in a single year, and capturing the world’s attention as Chinese EdTech’s commanded billion dollar plus funding rounds. India saw it’s own surge in funding in 2020, however China boasted a broader base of unicorns at the time and a more sustained run-up in funding when it first overtook the US in 2015 and invested over $25B of EdTech VC through to the start of 2021.

China’s clear EdTech investment leadership position rapidly unravelled through 2021 as the Chinese government initiated a broad range of policies that undermined the fundamental model accelerating EdTech in the country. Chinese companies teaching academic curriculum must go non-profit, cannot pursue IPOs, or take foreign capital. All vacation and holiday curriculum tutoring is off-limits, online tutoring and school-curriculum teaching for kids below six years of age is forbidden and agencies must not teach foreign curriculum or hire foreigners outside of China to teach. Listed companies are prohibited from issuing stock or raising money in capital markets to invest in school-subject tutoring institutions, and foreign firms are banned from acquiring or holding shares in school curriculum tutoring institutions. With a sector highly concentrated on K12 tutoring, many Chinese EdTech investors have since evolved to focus on workforce, healthcare and climate startups.

China’s $8B investment collapse was offset in the main by a massive $6B surge from the United States as a highly diversified and generally more mature cohort gained the support of investors new and old to meet the crisis come opportunity to support education and workforce on a broad based digital transformation. The US EdTech VC market was previously defined by two steady five year periods of growth, peaking in 2015 with the acquisition of Lynda.com by LinkedIn and again in 2020 as now household brands such as Coursera, Duolingo and Udemy powered into the pandemic with strong momentum, each of these examples rising to IPO through 2021.

2021 would also see Europe EdTech rise from a prolonged period of strong, stable and steady growth, but still grossly underweight venture investment, in a regional context once dominated by centuries old publishers and institutions. The pandemic proved a powerful accelerant for Europe EdTech achieving large scale momentum and early stage escape velocity. Platforms such as GoStudent, Multiverse,Labster and Open Classrooms set new investment records for the region and broad base European investors.

EdTech has seen 38 Unicorns so far, with 17 joining in 2021 alone, 5 IPOs in the last 12 months and one acquisition in 2015. The remaining 32 have raised $27.4B at a collective $97B valuation.

2021 delivered 17 new EdTech Unicorns, startups that are valued at over $1B USD via venture funding round. This is more than 3x the number added in any previous year and brings the 2021 year end total to 32. 2021 also saw five Unicorns escape the herd, making their way to the capital markets via IPO, 3 US Unicorns and 2 Chinese listed on the NYSE and NASDAQ, adding to the acquisition of Lynda.com in 2015 marks 6 Unicorn exits in total so far.

We are yet to see the impact of 2021’s regulatory changes on the Chinese Unicorn cohort but expect a number of acquisitions, Hong Kong or Shanghai IPOs or even closures as there is little doubt those valuations are materially impaired.

No items found.

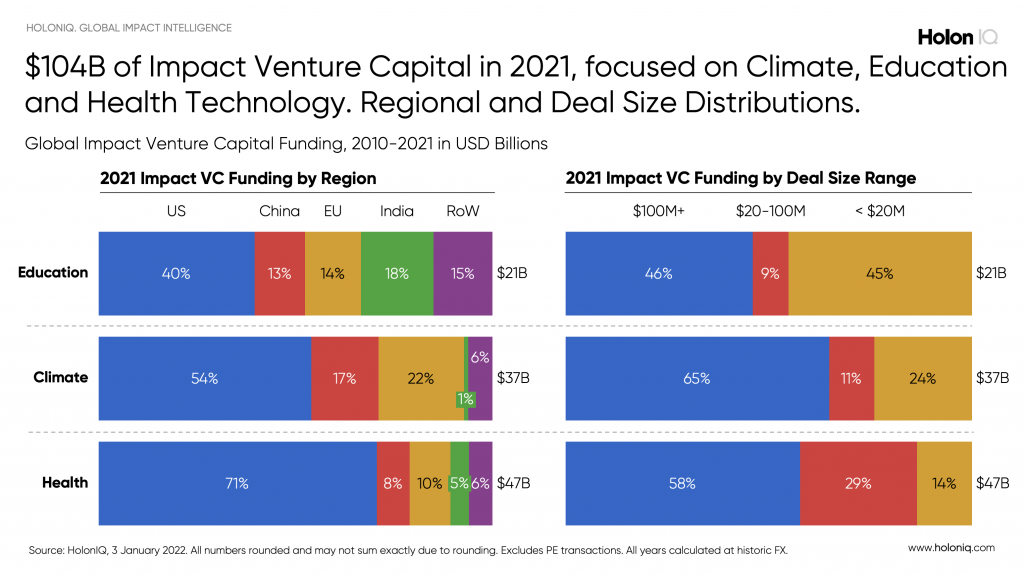

Impact Investing and a broad trend towards the United Nations SDGs, ESG and responsible investment is fueling a stronger supply of growth capital for EdTech alongside impact peers in Climate Technology and Digital Health.

Impact investing, the broad wave of focus on Environmental, Social and Governance (ESG) investment considerations, combined with rising awareness for the United Nations Sustainable Development Goals (SDGs) has created a new consciousness about social and economic impact.

Education is now a core focus area for the global investment community, alongside peer industries such as Climate and Health, together allowing investors to participate in the growth of this special cohort and positively contribute towards a more sustainable and inclusive future.

Impact Venture Investment in 2021 reached $104B, EdTech securing over $20B, ClimateTech $37B and Digital Health $47B. Each of these industries has achieved more than 40% CAGR in Venture Capital investment since 2014, Climate growing at 50%.

Global EdTech has much higher geographic investment diversification thanks to stronger regionalization characteristics than Climate Tech and Digital Health. Category leaders in EdTech and new ideas enjoy strong funding, but scale-ups lack the same capital support in EdTech than Climate and Health despite much less capital intensive models in aggregate.

Benchmarked against impact peers, Global EdTech funding has the highest level of geographic diversification. Outside of the US, Climate Tech has strong investment in China and across Europe but lacks the same funding support in India and across the rest of the world.

Mega Rounds dominate funding in all three industries ranging from 46% of all funding dollars in EdTech through to 65% in ClimateTech.

EdTech also boasts the largest share of early to mid stage investment in sub $20M venture rounds, almost as much of the share of dollars as the EdTech mega rounds, 2x the share of Climate Tech and 3x Digital Health. Given the different sizes of these industry groups, this does equate to a similar dollar level of investment across the three but does reflect a bias of funding towards more mature companies.

No items found.

Latest Insights

Global Insights from HolonIQ’s Intelligence Unit. Powered by our Global Impact Intelligence Platform.

We provide you with relevant and up-to-date insights on the global impact economy. Choose out of our newsletters and you will find trending topics in your inbox.

.png)